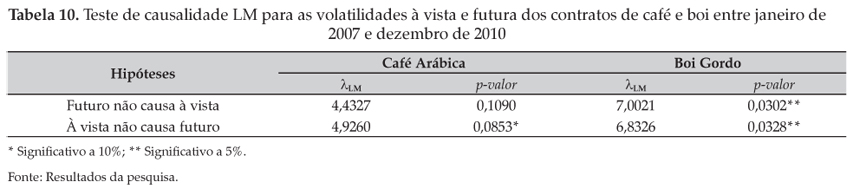

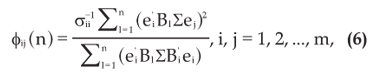

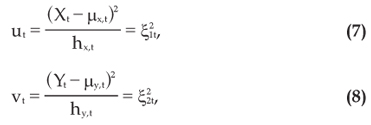

The bullish movement in commodity prices during the 2000s can be explained based on structural and conjectural factors. In addition, it was argued that this price movement was amplified by the contagion from the derivative markets. In this context, these contracts were one of the aspects responsible for an increase in cash price volatility. Thus, this paper evaluated the influence of trading activity (volume and open interest) and futures price volatility in spot price volatility for arabica coffee and live cattle in Brazilian markets. Granger causality tests, forecast error variance decomposition, considering vector autoregression models, and tests of causality in variance, based on the cross-correlation function and on the idea of Lagrange multiplier were conducted. The results showed that, during the period considered, in most cases, an unexpected movement in trading volume and variability of futures prices changed the pattern of spot price volatility.

Futures markets; commodities; volatility; causality